Under the impact of factors such as the collapse of Silicon Valley banks and oversupply in the oil market, international oil prices suffered a severe setback.

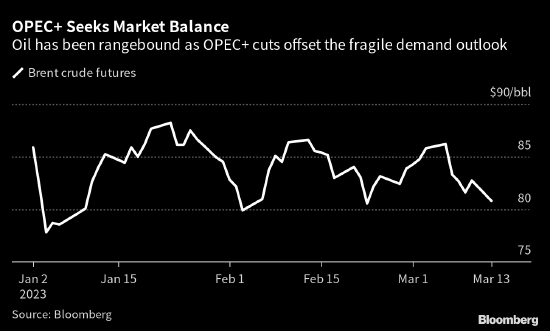

On March 14, international oil prices fell by more than 4%, hitting a new low in more than three months. The price of light crude oil futures for April delivery on the New York Mercantile Exchange fell 4.64% to close at $71.33 per barrel; Brent crude futures in London fell 4.11 percent to settle at $77.45 a barrel. On March 15, international oil prices continued to decline, and WTI crude oil futures once fell below $70 in intraday trading, hitting a 14-month low.

Although the oil market is under pressure from oversupply in the short term, the good news is that the outlook for crude oil demand this year remains somewhat resilient. On March 15, the International Energy Agency (IEA) raised global oil demand again in its latest monthly report on the oil market. It is expected that global oil demand will increase by 3.2 million barrels per day in 2023, reaching 103 million barrels per day. The IEA also warned that global oil supply may be in short supply in the second half of the year, unable to meet demand arising from seasonal trends and China's faster economic growth.

In contrast, OPEC’s monthly report released on March 14 was relatively cautious. Although it further increased its forecast for China’s oil demand growth in 2023, it maintained the global oil demand growth forecast unchanged, saying that global economic growth has potential downside risks.

Impact of the Silicon Valley Bank incident

The recent Silicon Valley bank failure storm has brought new shocks to the international oil market. In its monthly report, the IEA pointed out that with the collapse of Silicon Valley banks, people's concerns about the macro economy have intensified, and oil prices were once again negative in March.

From another point of view, the problem of Silicon Valley Bank will also affect the follow-up policy of the Fed. In March, there is a high probability that the interest rate will only be raised by 25 basis points, while the original expectation is 50 basis points. The cooling of tightening expectations is beneficial to oil prices. On the whole, the Silicon Valley bank turmoil has both advantages and disadvantages for oil prices. Some factors drive down, while others drive up.

Oil market faces short-term pressure from oversupply

In addition to the impact of the Silicon Valley Bank turmoil, from the perspective of supply and demand fundamentals, the short-term pressure on the oil market is not small.

Although the oil market is expected to be in short supply in the second half of the year, the IEA pointed out that the market is currently struggling with oversupply, with inventories rising to the highest level in 18 months. Global oil inventories surged by 52.9 million barrels in January to nearly 7.8 billion barrels, the highest level since September 2021, and preliminary indicators for February point to further builds.

OPEC also expects that the global oil market may experience a modest supply glut in the next quarter amid seasonally sluggish demand. The global demand for OPEC oil in the second quarter was 28.62 million barrels per day. If OPEC maintains the production level in February, it will be about 300,000 barrels higher than the daily demand. Global oil consumption tends to slow during the second quarter, which falls between peak winter heating and summer driving season.

In its latest monthly report, OPEC sharply raised its estimate of Russian supply for the current quarter. Although Russia is subject to Western sanctions and plans to cut production in response to the West, overall supply from Russia remains surprisingly strong. OPEC expects Russian oil production to reach 10.9 million bpd this quarter, about 620,000 bpd higher than forecast in last month's report.

If Russia's production continues to show resilience, the oversupply in the oil market may become more serious. However, OPEC currently assumes in its outlook that Russian oil production will drop sharply by 900,000 barrels per day in the next quarter, a decline even greater than that of Russia and Ukraine a year ago. When the conflict just broke out.

On the demand side, OPEC predicts that world oil demand will increase by 2.3 million barrels per day in 2023, rising to a record high of 101.9 million barrels, unchanged from last month's forecast.

The oil market is still supported in the long run

Driven by the shale oil and gas revolution, U.S. crude oil production has grown by leaps and bounds in the early years. It is regarded by the outside world as a "mobile oil producer" that can compete with OPEC. The U.S. has a large amount of idle production capacity and can quickly adjust production to affect international oil prices.

However, with the advancement of energy transformation, shale oil producers are unwilling to invest in large-scale expansion of production. The lessons of blindly increasing production in the past are vividly remembered. Shareholders are also eager to "secure their pockets", and production capacity growth has begun to slow down. In 2022, 26 U.S. crude oil companies will repurchase and distribute a total of US$128 billion in dividends, but few companies invest in drilling and expanding production capacity.

This also means that the long-term supply outlook of the oil market is worrying. OPEC Secretary-General Al Ghais warned that although Saudi Arabia, the United Arab Emirates, and Kuwait have formulated long-term plans to increase production capacity, OPEC alone cannot meet global supply demand. Other oil-producing countries must increase investment in drilling, otherwise the world will face energy security problems in the future.

The lack of supply will also support oil prices. Rick Muncrief, chief executive of shale oil producer Devon Energy, believes that as global supply capacity continues to weaken, the balance between oil supply and demand will tighten, and a new surge in oil prices may occur.

However, investors cannot ignore the impact of the Fed's continued interest rate hikes. As the impact of tightening policies gradually emerges, demand for crude oil will also come under pressure. The Fed's tightening policy has led to a tightening of US dollar liquidity, and the US dollar exchange rate is in a relatively strong position. It is relatively more difficult for non-U.S. countries to obtain U.S. dollars. Crude oil importing countries will be affected by the lack of U.S. dollars when importing international crude oil measured and traded in U.S. dollars, which will inevitably inhibit the demand for crude oil.

COMPANY: QINGDAO OWELL IMP&EXP CO.,LTD

E-MAIL: info@owellindustries.com

TEL / Whatapp: 0086-18561506730

ADDRESS: BLDG A, Qingdao Int'l Innovation Park, Qingdao, PR China

Copyright © 2020 Owell Industries All Rights Reserved. Site map